With all credit to Mark Collie and his great country song Trouble’s Coming Like a Train, he vividly depicted the urgency of the current domestic and world market conditions for anyone willing to do a little analysis and study financial history.

“Woke up on the wrong side this morning,

Thunder rolling in my brain,

Walked into an empty closet didn’t find a thing,

Trouble’s comin’ like a train. . .

Trouble’s comin’ I can feel it way down in my bones,

Trouble is I never fail to derail when I’m left alone,

Callin’ out my name, trouble’s comin’ like a train.”

Unfortunately, I rate this article as factual and one of the least enjoyable I have researched and written.

James Carville, Profit of Doom

I am not a fan of James Carville, but he is famous for a memorable quote from Bill Clinton’s 1992 campaign that has been used repeatedly in Politics. Carville’s famous “It’s the economy, stupid” was born and still resonates in politics and broader society. At the time, Clinton was running against George H. W. Bush, who made the mistake of promising no more taxes and then having to go back on that commitment. The country was tipping into a recession and ready for change.

As much as I dislike Carville, his observation was correct. He gave voters something tangible and impactful to focus on. Clinton won, and Carville’s ability to clarify the differences between Clinton and Bush was one reason.

The 2024 Election

We face an analogous situation going into the 2024 election cycle. Most people focus on the domestic economy when they should look broader at the world stage. While we are focused on the disasters brought on by the President, Congress, the FED, and Washington bureaucrats, our adversaries see our confusion, weakness, and opportunity. The potential impact of the 2024 election on our global standing cannot be overstated, and if we stay on the current path on all fronts, I see few long-term positive outcomes.

This time, “It’s the economy, stupid!” is one of many issues. While our media has been gaslighting their audiences over President Biden’s decline, the Hunter laptop scandal, Biden family corruption, transitory inflation, gas prices, reserve currency status, Supreme Court decisions, and a host of other issues, our enemies have been watching.

The 2024 election may be decided on petty and inconsequential domestic issues while the actual adversarial moves are taking place on a much larger stage. Financial storms are gathering in Europe, Africa, South America, and Asia; we need to know how they might affect us at home. There are plenty of domestic financial matters to be concerned about, but they are short-term if we address them now.

Our adversaries are working to reset our position on the world stage. Unfortunately, our politicians lack the understanding of international finance to act or do not want to acknowledge the problems. U.S. politicians are focused on reelection, not protecting our world standing, highlighting the urgent need for better leadership in Washington. This is it if there were ever a need for statesmen rather than politicians.

The Real Domestic Issues

Please do not think I am saying all issues are international; our politicians have dug a hole for us to climb out of, which is a significant challenge. I believe the Democrats and Republicans both welcome Hunter Biden’s gun and tax issues and President Trump’s issues because they distract the public from their gross financial incompetence. Corruption is easier to understand than economics and much more fun to speculate about.

No politician will stop Medicare, Medicaid, or Social Security because it would be political suicide. Nor can any of these go bankrupt so long as the FED can print money to buy Treasury debt. These are nothing more than political theatre used to sew fear and uncertainty to gather votes. These are an issue with our national debt, but that is another kettle of very smelly fish. They are tightly correlated but have different issues.

National Debt

Our national debt is front and center daily in the media or when we visit any store. It has risen massively, causing inflation felt by us all. It does not matter whether you are wealthy or poor; inflation destroys the dollars in your pocket like a silent tax. Money poured out during the pandemic and immediately after that settled into the economy, with no way to extract it without triggering a deep recession or depression. The cause started with the pandemic and ended with pure vote buying.

In addition, President Biden’s forgiveness of student loan debt and the open border have caused the debt to spiral out of control. Both moves are aimed at vote buying or political moves to reset the House of Representatives party composition. Student loan forgiveness is a direct hit to the debt, and the open border cost is hidden mainly because it taps into existing programs and depletes them of funds.

If you read and ponder this article for ten minutes, the national debt will grow by $90 million while you do so. Our national debt is so large that most of us cannot grasp the numbers, and it does not matter until the day it does, and then it is too late.

Interest Rates

Inflation from uncontrolled spending has forced the FED to raise interest rates to slow or reduce inflation. This has worked partially but caused even more significant problems. The interest on our national debt now exceeds all other expenditures and is compounding as we continue to borrow more daily to pay today’s and tomorrow’s interest.

Interest rates also reverberate throughout the economy, from bank bond losses to personal loans to mortgages to bankruptcies. A rise or fall in interest rates touches everything. When the FED sets the Federal Funds rate, it creates a floor from which all other rates are calculated. If you are a net saver, you look at this as some welcome relief, but most Americans are now net borrowers, and the interest rate shift hurts. The only saving grace here is that mortgage rates cannot go higher for most borrowers who held on to their existing fixed-rate mortgages.

Bank losses

The Fed and Congress have us on a razor’s edge, and no one knows to which side we will eventually fall. If the Fed lowers rates, it helps finance the national debt (slightly) and raises the value of the bonds the banks hold at a loss. The banks need this relief because without it, they are undercapitalized, and any severe downturn can cause another 2008-type banking crisis and require more bailouts. I would not doubt that the FED could lower rates so the banks can liquidate their bonds and then raise them again as inflation again rears its ugly head.

Lowering interest rates threatens to kick off inflation at an even higher level. If the FED lowers rates, it is purely a political move for the election, and they will need to raise them even more after the election.

Personal and Household Debt

The money passed out during the pandemic and after might go down in history as the greatest bonehead move in the country’s history. We now have too much money in circulation and a populace addicted to spending even more than before the pandemic. Household debt for cars, trucks, and household goods is at an all-time high. However, so much money is circulating that consumers will keep spending as long as banks extend credit to them. We have a consumer-driven, debt-dependent economy, and if we stop the merry-go-round, the actual size of the problem will come roaring at us like that train.

We also have a Congress unwilling to admit our dire circumstances and to take the necessary steps to correct them. To do so, they must admit they are a significant cause of the problems in an election year. We also need to understand that most of Congress lacks the training to comprehend what they have done, much less the solution. Sadly, many Congress members seem to have replaced the Post Office as the employer of last resort.

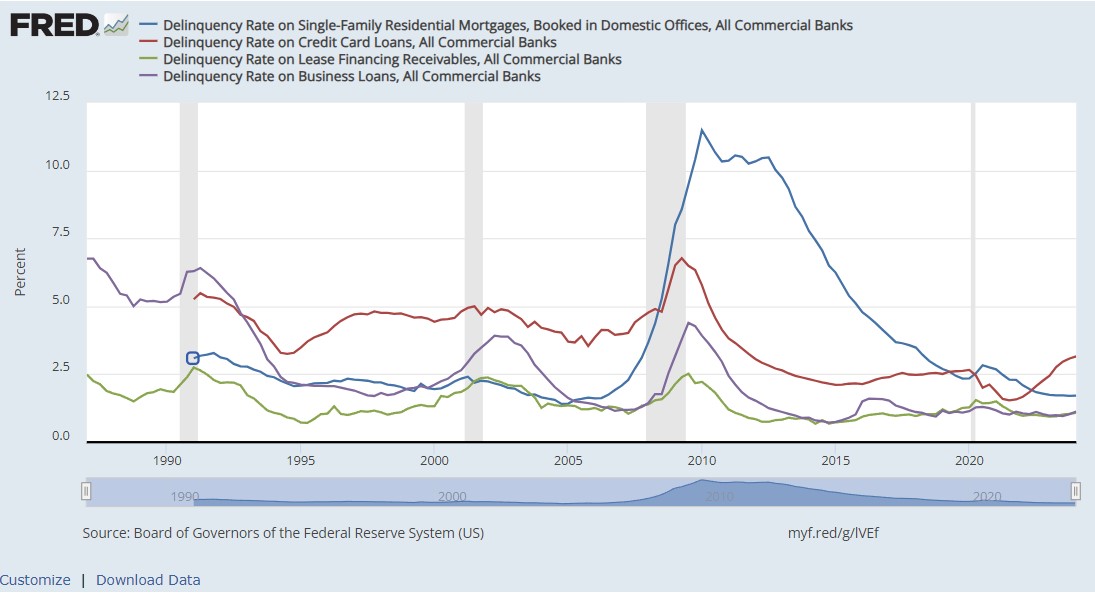

Delinquencies and Bankruptcies

Mortgage, auto, and personal loan delinquencies have risen in recent months. This is one of the early indicators that the economy is stagnating or starting to decline. Most consumers will pay their mortgage and keep their car until they cannot afford it anymore, so when these delinquencies and related foreclosures and repossessions start to rise, it is a bad signal for the economy.

None of the delinquency rates are at a crisis level yet, but all delinquencies have turned higher. The pandemic money helped delay delinquencies for all borrowers, and President Biden’s Student Loan delays and gifts have artificially knocked down those delinquencies. Eventually, things begin to normalize, and borrowers who cannot repay their debts are exposed. Shifting the debt to the Federal Government and then to taxpayers does not solve the problem; it delays it and makes it unfair and worse.

Commercial Real Estate

There is a lot of noise in the news about the crisis in real estate mortgages. Several factors come together to make this crisis. First, most of these loans are “interest only” loans where the borrower only pays interest to the lender. This works fine as long as the property always increases in value. However, the second issue is that the pandemic and new trends in remote work now have borrowers in a position where they have fewer renters, values are dropping, and there is no way to repay the loans. Third, many of these loans are made outside the regulated banking system, so the quantity of the loans, the strength of the borrowers and lenders, and loan terms can be unknown. Fourth, these loans often make their way into the markets for funding through mortgage-backed securities, and delinquency rates have tripled this year, with much more to come. Commercial Real Estate prices have fallen into negative territory for the first time since the Great Recession in 2008.

Unemployment

Depending on who you listen to, unemployment rates are still in a good range, or the Bureau of Labor Statistics cannot count. According to the Federal Reserve, layoffs have started to climb, especially in the Tech Sector. This is unusual, given all the talk about artificial intelligence, building out data centers, and cyber security needs.

International Issues

On the international front, there is little to feel good about. We have the BRICS Consortium, trends by central banks with gold purchases, the U.S. dollar reserve currency status, the Ukraine War, and the war in Israel. The international scene is worth another discussion, but you can feel the additional weight on everyone and everything.

It’s the Momentum, Stupid!

When I was growing up, we had a passenger train called the Silver Comet that would come through town twice weekly on a circuit from New Orleans to New York. We would put pennies on the track just before the train arrived and search for them after the train departed. The pennies would be flattened but not unrecognizable, just unusable. The accumulated weight of the engine and cars ensured that nothing survived as it had been.

If you have ever been in a station when a train arrives, you understand the power and momentum of significant events. When a train arrives, the ground shakes, the tracks clear, and unique sounds and smells that only go with trains are everywhere. The size and presence of a train communicates that you do not want to be in front of it when it arrives or leaves the station. And so, it is with seismic shifts in the economy and world events. You want to understand and prepare for them, but not stand on the tracks.

Our politicians like to interpret economic events and changes so that the sum of their bad decisions is never discussed. But the momentum of their bad decisions is building, and when they arrive, it will flatten everything on the tracks. Maybe we can ask James Carville to stand on the tracks and yell, “It’s the momentum, stupid!”

Resources

Americans felt shakier about the economy in June, By Alicia Wallace, CNN, cnn.com, June 25, 2024.

Broken Money: Why Our Financial System is Failing Us and How We Can Make it Better, By Lyn Alden, Timestamp Press, amazon.com, August 25, 2023.

CMBS Delinquency Rate Surges Back Above 5% in June with Three Property Types Posting Large Increases, By Stephen Buschborn, Trepp, trepp.com, July 2, 2024.

Consumers haven’t felt this bad about the economy since November, By Elisabeth Buchwald, CNN, cnn.com, May 10, 2024.

Credit Card and Auto Loan Delinquencies Continue Rising; Notably Among Younger Borrowers, Federal Reserve Bank of New York, newyorkfed.org, February 6, 2024.

FRED Economic Data, Commercial Real Estate Prices for United States, Federal Reserve Bank of Saint Louis, Last accessed July 3, 2024.

How Fear of Regret Influences Our Decisions, By Geoffrey Engelstein, The MIT Press, thereader.mitpress.mit.edu, February 26, 2024.

It’s the economy, stupid!, Wikipedia, wikipedia.org, Last accessed July 2, 2024.

Losses Pile Up in Top-Rated Bonds Backed by Commercial Real Estate Debt, By Carmen Arroyo and Natalie Wong, Bloomberg, bloomberg.com, May 23, 2024.

Mortgage Statistics: Historical & Current United States Residential Mortgage Origination & Loan Servicing Statistics for 2024, Mortgage Calculator, mortgagecalculator.com,

Mortgages 90 or more days delinquent, Consumer Financial Protection Bureau, consumerfinance.gov, Last accessed July 3, 2024.

The FRED Blog: The lowdown on loan delinquencies, FRED Economic Data, Federal Reserve Bank of Saint Louis, Last accessed July 3, 2024.

Trouble’s Comin’ Like a Train, by Mark Collie, SongLyrics, songlyrics.com, Last accessed July 3, 2024.

Trouble’s Comin’ Like a Train, by Mark Collie, YouTube, YouTube.com, Last accessed July 3, 2024.

What the Science Actually Says About Unconscious Decision Making, By Ben R. Newell and David R. Shanks, The MIT Press, thereader.mitpress.mit.edu, September 22, 2023.

Why Having Too Little Leads to Bad Decisions: Financial stress leads to a downward spiral of bad decision-making, By Denise Cummins, Ph.D., Psychology Today, psychologytoday.com, September 26, 2013.