I watched CNBC this morning and had to remind myself that they have an agenda and are selling a position aligned with the Democrats. I am not sure they even recognize how biased they are anymore. Their positions on many things are so far off track that a one-semester economics student can make better predictions about inflation and interest rates. If we hear the “Inflation isn’t that bad, and it is getting better.” any longer, we will all need some Prozac to make it through the day.

The most reasonable and common-sense anchor on the show is Becky Quick. She makes just $3 million annually and has an estimated net worth of $20 million. She is a pauper by Wall Street standards but at least tries to understand that not everyone has a six—or seven-figure salary, and inflation is real to the rest of us.

Blindly trusting their advice and forecasts would require us to believe that two thousand years of economics are suddenly irrelevant. The latest inflation data is a stark reminder that it’s here to stay, and the irresponsibility of Congress has put us in a tight spot. Congress’ inability to curb spending for fear of losing votes is a ticking time bomb for our economy. Unfortunately, we are in election season, and they are more concerned with the next election than the long-term economic implications of their actions, leaving the mess for the next set of officials to clean up. If you are a Democrat, you might want to lose this round so that the Republicans inherit the mess.

Everyone cannot be an economist, but someone in Congress should at least be able to add, subtract, and balance a bank account. Unfortunately for those of us out here in the real world, their actions have real kitchen table implications. Inflation is real, an over-hyped and over-stimulated stock market is real, and the risk is now being reflected in world economics and commodities like gold. The gas and food price increases are real, not just a statistic to be debated by politicians and economists.

What is happening with gold?

In the past few weeks, I have heard several debates on gold and silver prices that are all over the board. Gold advocates believe that as the currency weakens through Congressional actions, gold can only go up to $2,500 or more. Still, gold advocates have been saying this for decades with little rapid price movement until now. The price has now risen to over $2,400 before retreating slightly. It will go higher, but when is always the question. We need more time to understand what is happening with wars, economics, and politics to know if the move is permanent or just another knee-jerk reaction to world events. But for now, gold and silver are up in a meaningful way.

In one of the strangest moves in financial history, the Fed started sending monetary gold standard signals last month. As noted in an earlier article, this would expose how badly Congress has devalued our currency, so it has no chance of going anywhere. If the FED were to push harder, Congress would vote to move the FED inside the government to block any such moves.

However, the article and interview are worth considering. First was a report from the Philadelphia FED explaining price levels under the gold standard. Unless you are an economist who enjoys esoteric financial math, I would skip this one. But there are summaries that cut through all the math.

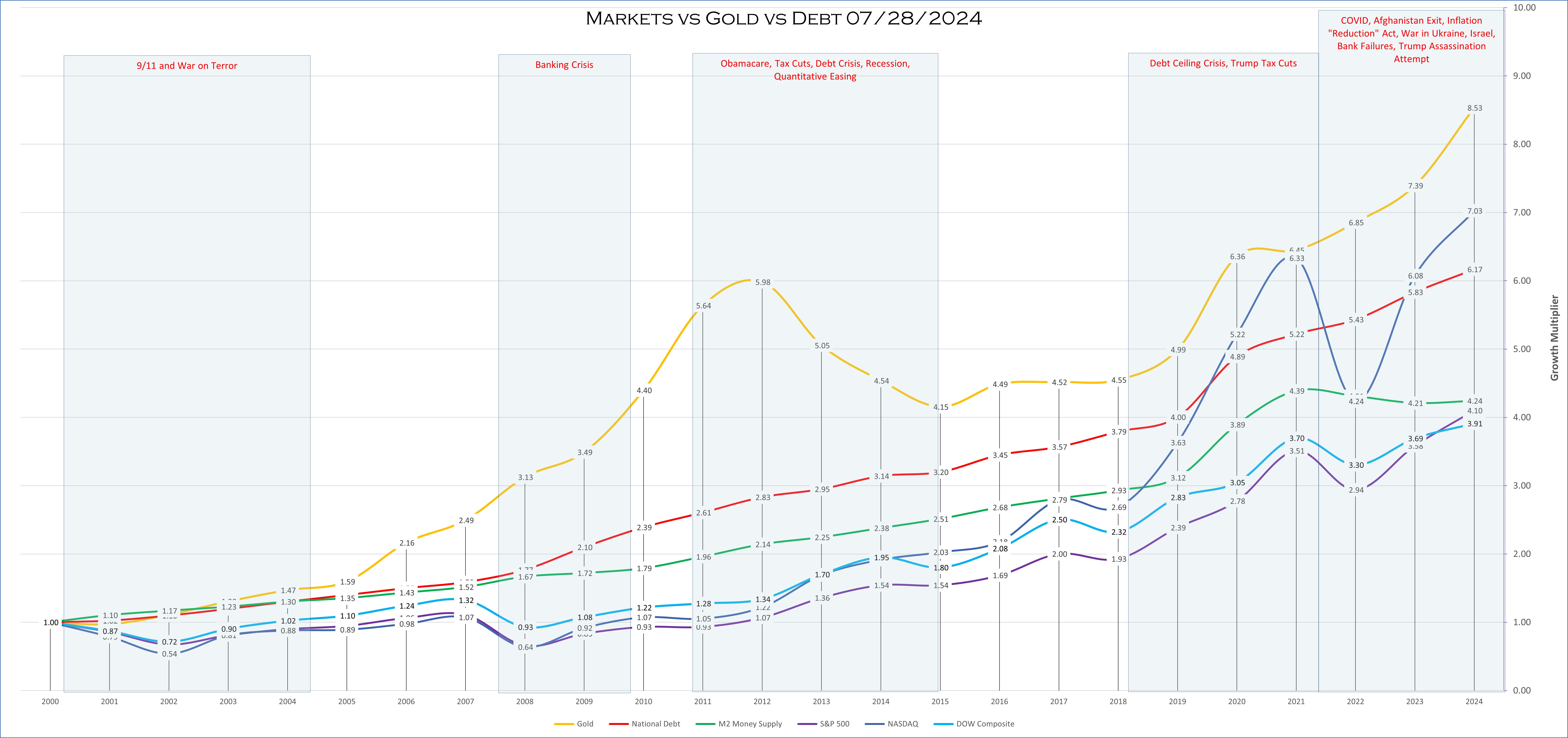

The Long View

The long view is for those who hit our peak earnings in the early 2000s. This view is most relevant to Baby Boomers in the investing world and overlaps the other two periods we discuss here.

In the long view, from 2000 until today, gold remains the only asset that outperformed all the markets and the growth in the national debt over the whole period. The NASDAQ has held up, but only because of a handful of stocks and the irrational exuberance over AI. There are discussions about “coming to our senses” about AI, which could cause the NASDAQ and S&P 500 to moderate. If the markets begin to bring AI discussions into the real world, even the NASDAQ and other market averages could dip. This morning, I received an email from Samsung advertising AI versions of washers, dryers, refrigerators, and ranges. For a mere $7,500, you can replace your appliances with Wi-Fi-connected, thinking ones, a discount from the normal $10,000 price tag. The oven even had an internal camera to watch the brownies bake or burn. Irrational exuberance is here! When we become so lazy that we cannot walk into the kitchen to see if the turkey is done, technology has reached the absurdity level.

However, the national debt will not moderate since the FED had to keep rates higher for longer to curb inflation. I believe any attempt to moderate rates is only election engineering and risks stimulating inflation even more. Smaller moves in rates will not help the economy, nor will they moderate the soaring cost of our debt.

The FED is swimming upstream in its efforts to rein in Congress’s spending, but it may be a futile attempt to rescue the dollar against the winds of change. They are reining in their balance sheet and trying to offset the spending by Congress, but the national debt and inflation are the silent killers. The FED’s efforts to slow things down are visible as they reduce the M2 Money Supply. Is it enough or too little, too late? Only time will tell us that answer.

I believe the real killer for all of us is the fading prestige of the dollar on the world financial stage. That is a much longer discussion for other articles, and the BRICS movement is at the heart of the matter.

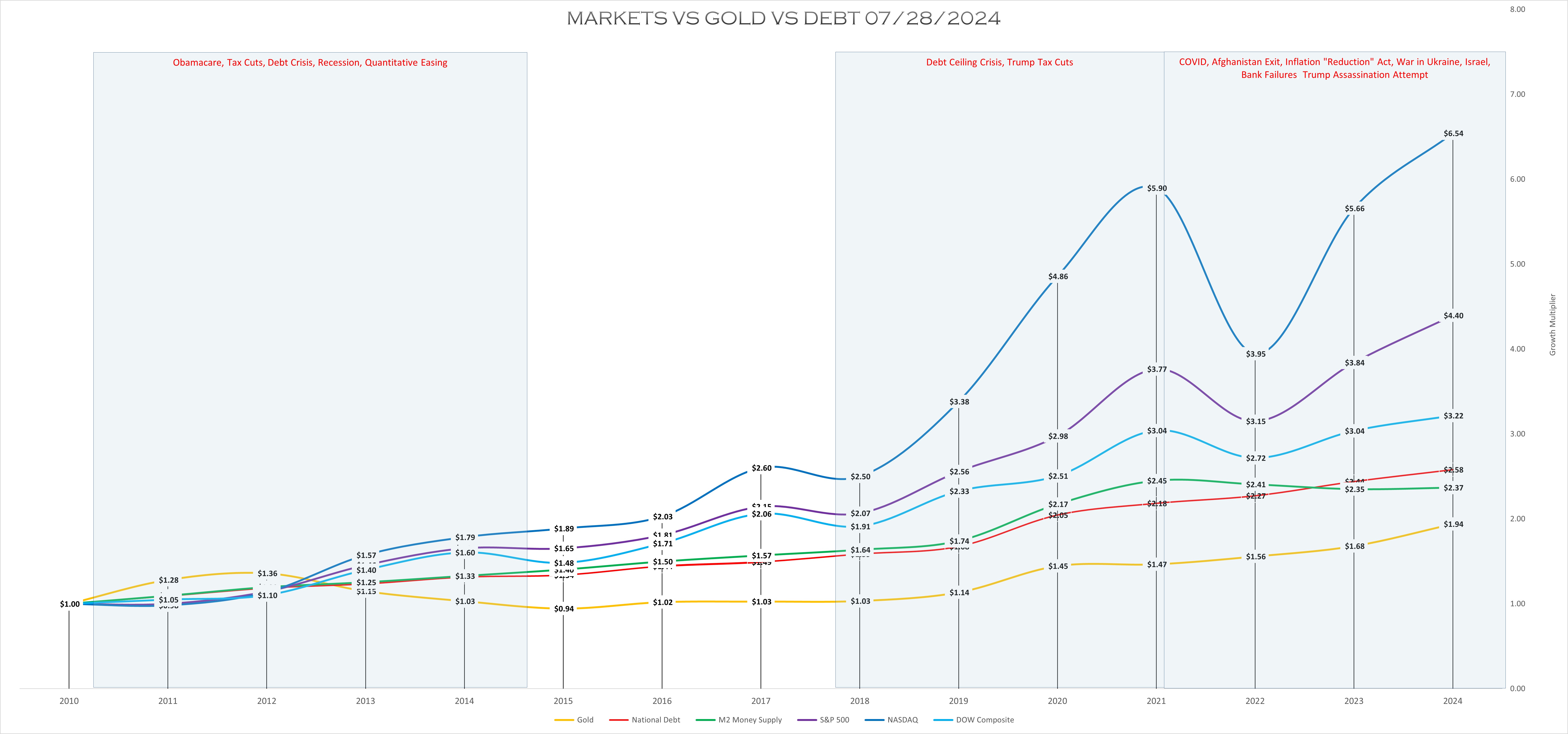

The Medium View

Nothing has changed significantly in our Medium View of Markets, and it continues to say almost the opposite of the Long View. Gold rose from 2010 until today but did not exceed market growth in other areas. The gold connection to the national debt is still apparent. The FED’s attempts to shrink the M2 Money Supply are also more evident in this chart. Without severe corrections in the National Debt, the gold/National Debt connection likely continues upward. We are nearing a point of no return with the National Debt where it exceeds all other spending by the Federal Government. The challenge for the FED is to pull us back from the brink without triggering more than a mild recession.

We do not want to become another Japan with out-of-control spending and debt, coupled with stagnant long-term GDP growth. However, we also have the same population issues as Japan and China, with low birth rates and a ballooning older population. Eventually, our population will start to decline without controlled immigration, making payments on our debt unsustainable.

Starting points for these calculations also matter. In 2010, the DOW had dropped from its 2008 high of 13,000 down to 10,000, so for these calculations, the markets are at a low starting point, thus making their growth seem stronger. Calculating from the 2008 highs would make the charts look more like the long view.

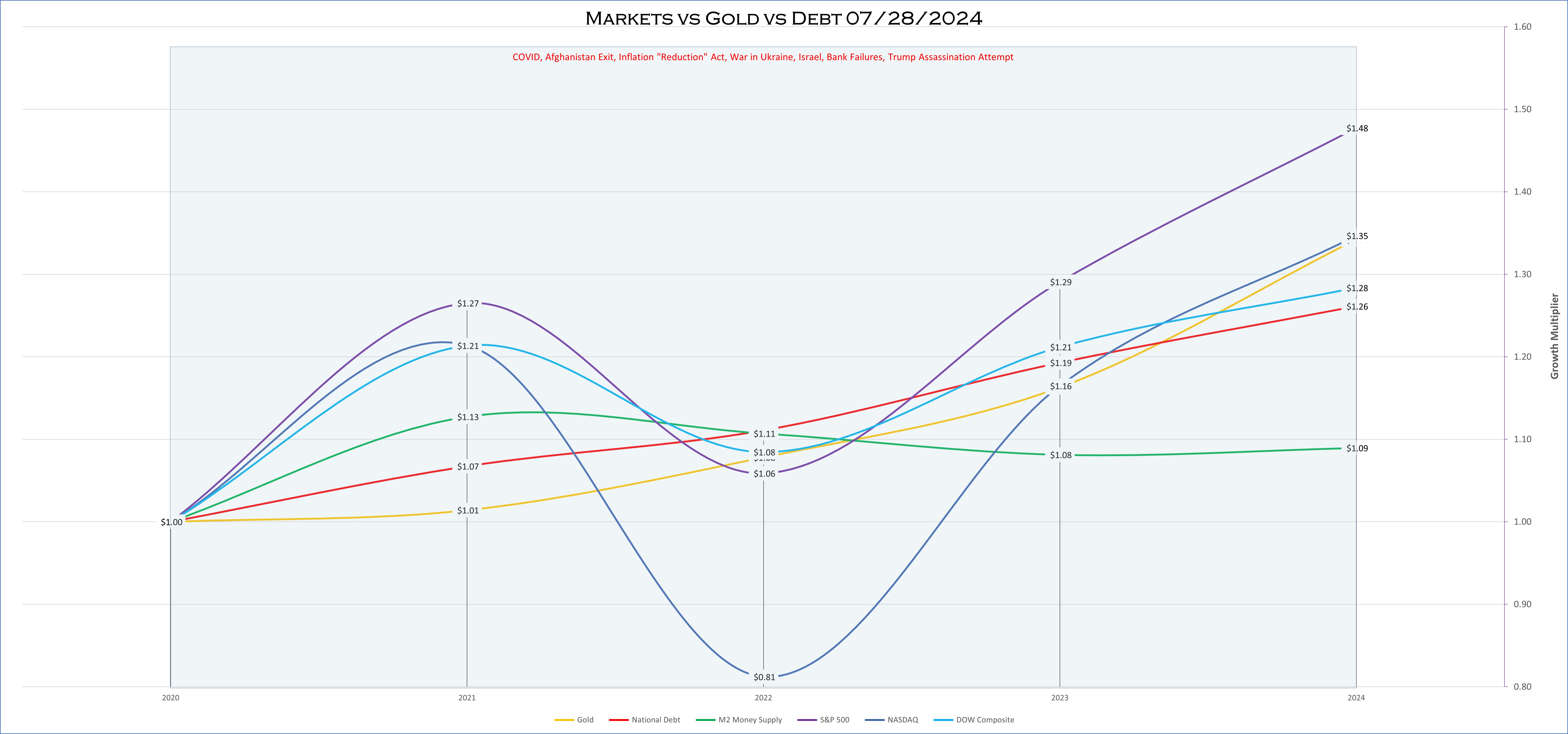

The Short View

Our Short View of markets now looks slightly more like the Long View, with gold starting to outperform stocks. Gold is still correlated to the National Debt and has started moving up faster. I believe gold will hold some premium because China, Russia, and India are on a gold-purchasing mission in concert with their BRICS effort and a need for stable reserves. Their effort to “dump the dollar” is gaining traction despite their financial struggles.

The “Magnificent Seven” (maybe the Super Six or Fab Five) stocks have started to cool a little, allowing gold to outperform all but the S&P 500 Index. I do not believe that gold’s run is over, and the next time we do this chart, it may look like the long view. The FED’s efforts to shrink the money supply and the rapid climb in the national debt are even more pronounced in this chart. As long as the FED and Congress keep passing out money, the BRICS nations keep accumulating gold, and the Administration uses our reserve status as a weapon, these trends will continue.

Central Bank Issues

The United States has the largest gold reserves, a holdover from the gold standard days and World War II. My best guess is that it just “feels right” for the United States, with the World Reserve Currency, to hold the world’s most significant quantity of gold. However, the Fed cannot hold rates up, curb inflation, finance debt, and keep the markets going forever up.

China and Russia want to dethrone the US Dollar as the reserve currency, and they are doing everything they can in markets to make this happen. The BRICS consortium is pushing for additional membership, and just this year, they have expanded their membership and participation to at least forty-one countries. These countries now represent about one-third of the world’s GDP. I believe we are seeing the world’s financial order sort into nations with raw materials versus producer nations with separate financial structures. Senator J. D. Vance, Trump’s running mate, has even expressed his doubt about the value of our reserve currency status. He believes our reserve position discourages domestic investment.

US Banking Issues

Our banking issues are directly tied to the sum of all these factors, but mainly debt in all forms. My experience tells me that as consumers and corporations reach their debt limit, a recession or depression always follows. Consumer debt in credit cards, student loans, HELOC loans, and buy-now-pay-later loans is unsustainable. Bankruptcies and delinquencies are rising, another early warning sign of financial issues. Another warning signal expressed by many is that the FED’s move to lower interest rates will signal the start of a recession.

Why Does All This Matter?

Decades ago, our financial issues took place primarily on our shores. Today, our challenges are interconnected to all economies, and some nefarious players want to supplant our system of government with their own. These nations and bad actors often see capitalism as a threat to their ability to control their people, and they seek to destroy it and us. It matters for our children and grandchildren, and we owe it to them to leave our Country and the world in better shape.

Resources Used in This Article

Forget FAANG, Meet the ‘Magnificent Seven’ Stocks Surging in 2023, by Mallika Mitra for money.com, Nasdaq.com, June 16, 2023.

Forget The Magnificent Seven. Focus On These Fab Five, by Ed Carson, Investor’s Business Daily, investors.com, February 5, 2024.

Gold Demand Trends Q2 2024, by World Gold Council, gold.org, June 30, 2024.

Magnificent 7 Stocks: What They Are and How They Dominate the Market, by Wayne Duggan, US News, usnews.com, January 16, 2024.

One chart shows how the ‘Magnificent 7’ have dominated the stock market in 2023, by Josh Schafer, yahoo!finance, finance.yahoo.com, November 15, 2023.

The Global Debt Bomb: Debt + Derivatives = Over 1 Quadrillion Dollars, from This $233 Trillion Bomb is Set to Blow, dailyreconing.com, by James Rickards, April 10, 2018, goldsilver.com, reprinted April 11, 2018,

The London Gold Fix: A Brief Guide, by gainesvillecoins.com, coinweek.com, August 3, 2022.

Who Really Controls The Gold Price?? The Answer is Quite Surprising, by SRSrocco, Gold-Eagle.com, April 28, 2017.