So much is happening in the world of domestic and global finance that summarizing my thoughts and concerns feels like swimming upstream in the River Styx. Many days, the news makes me want to whistle a little tune, like whistling while you walk past the graveyard.

At year’s end, taking a little time to look back at 2025 and to gird ourselves for 2026 seems wise. We hear conflicting news and signals, and confusion seems to be the norm. If you watch CNBC or FOX Business News in the mornings, you will think all is rosy. But, as we noted in an earlier article, this is true only for those on the “Arm of the K”.

In these choppy and dangerous waters, I am glad Scott Bessent is at the helm of the Treasury. I do not always agree with his assessments of economic issues. Still, I think he is intelligent and will make the best decisions possible given the information and options available. It is his job to paint an optimistic view of the economy, but I believe he sees the many sandbars just under the surface. If we come through 2026 whole and intact, he will deserve much, if not all, the credit.

Headwinds Abound

For the past four or five years, many have forecasted doom and gloom, only to see markets rise. I must admit that the little I know about economics has been screaming at me that a long-overdue recession is underway. But the pockets of recession never seem to grip the whole economy, and the Ship of State sails on, even if with torn and tattered sails. But my age and experiences from earlier recessions keep me on edge, with a healthy skepticism in perilous times. In this article, I will recap what I see, and readers can take it as they will.

National Debt

Above all else, looming for me is the size and growth of the national debt. Now above $38 trillion, it is unsustainable without a significant change to our lifestyle and security. As noted in an earlier article on Higher Taxes, we need to raise both corporate and individual taxes slightly to slow the rate of growth in the national debt.

I would not even suggest this if our alternatives were not even more dire. If we raise taxes on income, we isolate the damage and maybe slow the rate of growth. If we do not raise taxes, then the “silent tax” of inflation takes a portion of everything. But continuously voting to lower or freeze taxes is nothing more than vote harvesting by both parties.

In 2026, almost $10 trillion of our debt will mature, requiring refinancing. All of this will be at higher rates and will accelerate the debt crisis unless we act. We are already reaching a point where foreign nations do not want our debt because they see the waste and fraud embedded in our national finances. They have calculators and computers and can analyze our fiscal path. They do not like what they see, and their unwillingness to buy our debt will force us to monetize it, driving us closer to a financial and fiscal cliff.

I now have zero faith or expectation that either party will take the actions needed to begin to reduce the debt. The last time anyone in Washington had an interest in reducing the debt, Andrew Jackson was in the White House. Since then, all have talked about it and done nothing. So the best we can do as citizens is take the actions that we believe preserve our wealth and give us the best chance to weather the financial storm.

Vote Buying Season

With the midterms looming, we all know it is vote-buying season in Washington. So, the odds of Congress or the President taking action that would alienate voters are lower than my chocolate lab remembering my birthday.

It is much more likely that Washington politicians will go back to quantitative easing to increase market liquidity. They will find new tax breaks for seniors and other voting blocs. And I am sure they will make other moves that will fuel inflation post-election. In fact, Secretary Bessent just announced some “Balance Sheet Expansion” that others are characterizing as permanent and open-ended QE.

Naming things something other than what they are is a Washington skill that has no parallel.

Consumer Debt

A big bump in the superhighway of eternal economic bliss is consumer debt. While those in the “Arm of the K” can ignore this, the rest of us cannot, and it will eventually slow down consumers, lenders, or both. We are at record levels for mortgage, student loan, credit card, vehicle, and buy-now-pay-later types of financing. We can pretend there is no problem, but it is there, and it is starting to bubble to the surface in the form of delinquency. This is the leg of the “K” and the area of the economy that Wall Street either cannot see or chooses to ignore to keep the party going.

Commercial Real Estate

Everyone admits that there is a refinancing issue for commercial real estate. It is often referred to as a brick wall, a point of no return where both lenders and borrowers must reconcile their differences. Commercial real estate is often a business in which the borrower has very little capital invested in the property, and the lenders bear almost all the risk. This encourages the lender to engage in what is called “Extend and Pretend,” in which loans are refinanced, and everyone pretends everything is all right. This is one of the obvious “Whistling past the graveyard” issues for sure.

Complicating this is the source of financing, private equity and private lending. These lenders are unregulated, often more accepting of risk, and more susceptible to failure. The size of the problem and the health of the borrowers and lenders are accepted as unknown. The President and the Treasury are pushing for lower rates, partly because of this issue, and also to lower interest rates on our national debt.

Precious Medals

Nothing seems to occupy our time these days like the movement in gold and silver. For many, their upward trajectory signals the collapse of our economic system or serves as justification for beliefs in gold or silver conspiracies. For others, it is nothing more than a reflection of supply and demand trends and the natural movement of prices that reflect scarcity.

Take your pick; they may all be true. With history, especially financial and monetary history, more than one thing can be true at any point in time. More than one thing can combine to create market movements.

Gold

Many forces are combining to push gold to new highs. It is the perfect storm of intended and unintended action converging at just the wrong time. We have the rise of the BRICS nations, loss of confidence in the dollar, confiscation of foreign assets, tariffs, inflation, and a stock market where success is focused on a handful of stocks that many believe are wildly overpriced.

All of these factors combine to make consumers and investors nervous, and gold is an alternative they see to protecting wealth. The competition for gold is no longer just with consumers; it is with central banks, with almost all overtly adding to their stockpiles and many believed to be doing so covertly. In 2022, 2023, and 2024, central bank purchases exceeded 1,000 tonnes per year, doubling the previous year’s purchases. We know the BRICS nations want to undermine the dollar, and stockpiling gold is a way of creating reserves no longer tied to the United States. Gold becoming a tier one reserve asset also encourages central banks to hold it.

Gold demand in ETFs, coins, bars, and jewelry remains strong. The United States still holds the largest physical reserves, but China and Japan have the largest total reserves counting paper contracts. There is definitely a trend by central banks to now substitute gold for dollars as a primary reserve, and this seems unlikely to change with the rise of the BRICS nations and the uncertainty of our debt.

COMEX Silver

For decades, gold has taken the front row seat among metals, but now silver appears to be rivaling it for appeal and investment. Silver has become one of the primary topics of discussion and is universally present in online discussions. As always, precious metal enthusiasts think their moment in the sun, their long-awaited vindication, is here. We added silver prices to the charts, and they show a trend line that closely parallels gold.

There is an industrial use for gold, but not like silver. From solar panels to batteries to chips, we seem to have reached a point where silver mining cannot keep up with demand. Large banks have long held down the price of silver through short selling, but industrial use seems to have negated their ability to control it. You can find a price forecast from $65 to $650; take your pick. But for now, it seems headed higher and is worth following.

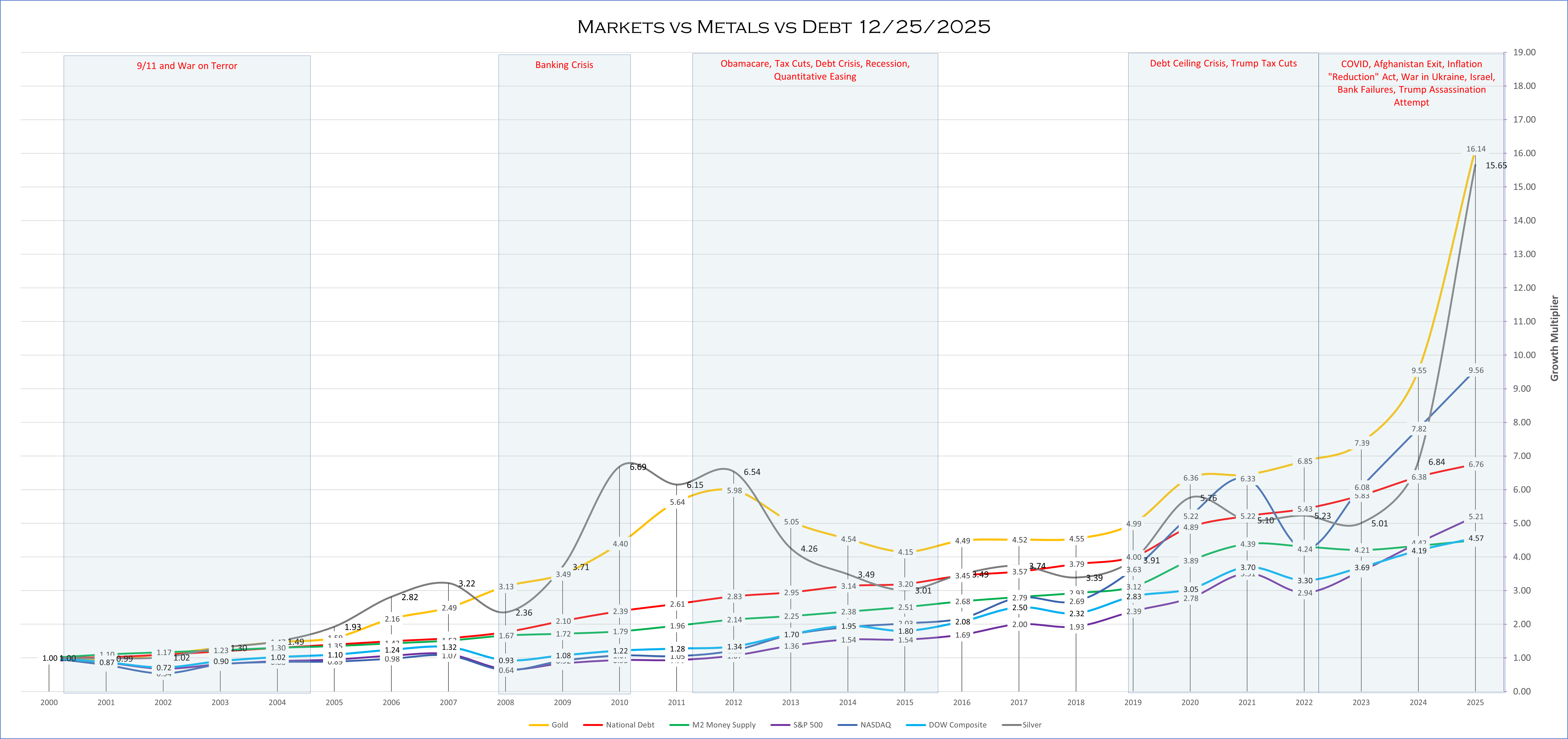

In these charts, it is evident that, when measured from either 2000 or 2020, nothing has matched the rise of gold and silver.

Platinum

Platinum, in recent years had become the forgotten metal. Platinum is widely used in catalytic converters, and with the net-zero and EV push, the need for catalytic converters was waning. But with changes in direction for many developed countries and consumer preferences, gas and diesel vehicles are back in vogue. This significantly increased demand for platinum, and the price has risen sharply, as could be expected. Platinum is a more detailed discussion for another day.

Markets and Metals

As we have done in previous articles, we take a long-term, medium-term, and short-term view of the market and metals. In this article, we focus only on the long and short charts due to the length of the discussion. But in 2026, we will again look at all three in future articles. As a reminder, this is purely a math exercise, but we think it is a fair one. There are untold ways to analyze the data and make arguments for inclusion and exclusion of factors, so we stick with the simple being best.

The straightforward question is: “If I had a dollar in 2000 or 2020 and I put it in one of the markets or metals, how much would I have today?”

The Long View

From 2020 until today, nothing has outperformed gold and silver in this chart. The unusual thing is that much of the movement in gold and silver has been parabolic, occurring over weeks and months, not years.

Where this will go and what it will mean for stocks, real estate, and metals markets is anyone’s guess. But things are changing, and as the BRICS nations bring pressure on Western markets, we can expect more volatility. The BRICS nations and others want to unseat the dollar as the reserve currency, so when they make moves is uncertain.

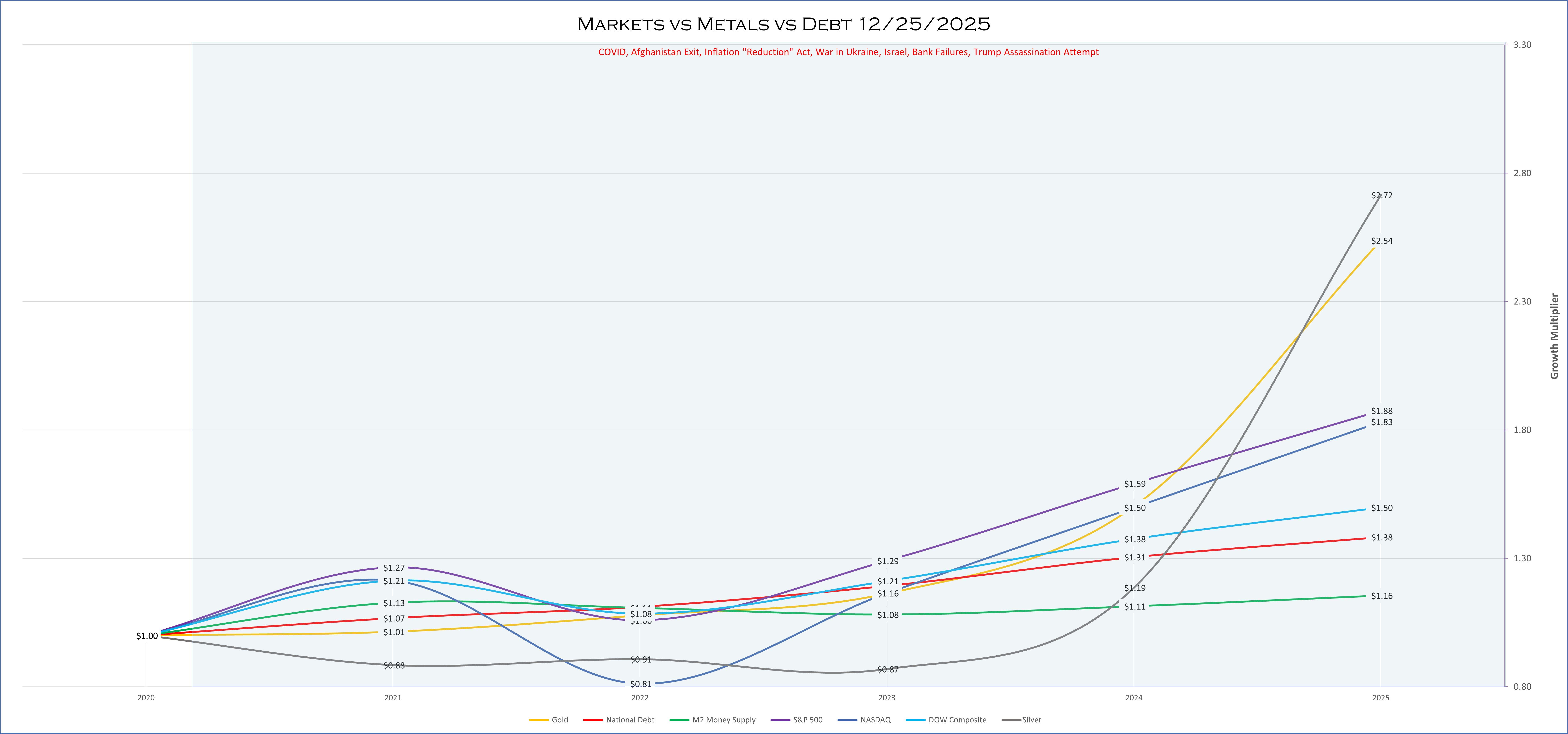

The Short View

Our Short-Term View of markets now looks slightly more like the Long-Term View, with gold and silver moving up rapidly. Briefly, before the election, uncertainty pushed gold to the same level as the S&P 500. Now that the “Trump Bump” is cooling off, we must continue looking at all markets.

As with the Long View chart, nothing has kept pace with gold and silver since their meteoric rise in 2025. Silver now outshines gold in this chart, and if predictions are even directionally correct, it will continue to do so.

Strange and Unusual Times

To me, this says a very different thing than I might not have asked in prior times. Last year or in 2023, I might have asked, “What is driving the price of silver and gold up?” Today, I would ask, “What is driving the value of the dollar down?” With silver, I believe you have to ask both, “What is driving the price up and the value of the dollar down?”

In recent months, we have seen the Yen Carry Trade disrupted as the Bank of Japan raised rates on its bonds. We are seeing moves by China to drive up the price of silver. We are witnessing dislocations in silver pricing between New York and Singapore, as arbitrage transactions cannot be executed due to shortages in silver inventories.

Then, on top of this, we are seeing new industrial uses for silver in batteries that will push inventory shortages to new levels and, theoretically, silver to even higher levels. How high? No one knows for sure, but the banks and brokers who are short silver in New York will do everything within their power to drive the price back down.

Between markets and metals, these are unusual times for which we have no playbook. It is a time for careful thought when investing and to seek the best and brightest advice you can find.

Resources and Additional Reading

2026 U.S. Debt Refunding and the Risk of Fiscal Shock: Navigating a High-Debt, Low-Liquidity Environment with Defensive Strategies, by Rhys Northwood, AInvest, ainvest.com, December 13, 2025.

8 Best Platinum Industrial Uses Every Business Should Know, Ledoux & Company, ledouxandcompany.com, January 13, 2025.

Charted: A Decade of Central Bank Gold Purchases, by Ryan Bellefontaine and Athul Alexander, Visual Capitalist, visualcapitalist.com, October 23, 2025.

Gold Reserves by Country, World Gold Council, gold.org, December 2, 2025.

H.R.5376 – An act to provide for reconciliation pursuant to title II of S. Con. Res. 14, Congress.Gov, congress.gov, Last accessed December 20, 2025.

Inflation Reduction Act, Wikipedia, wikipedia.org, Last accessed December 21, 2025.

Inflation Reduction Act: Preliminary Estimates of Budgetary and Macroeconomic Effects, PENN WHARTON, University of Pennsylvania, budget.model.wharton.upenn.edu, July 29, 2022.

QE eternity?, by Jon Faust, Center for Financial Economics, Johns Hopkins University, krieger.jhu.edu, December 16, 2025.

The Debt Refinancing Wall Ahead: What the Next Few Years Mean for Investors, DePalolo & May, dmstrategicwealth.com, May 21, 2025.

The Inflation Reduction Act Still Reduces the Deficit, by Bobby Kogan and Brendan Duke, The Center for American Progress, americanprogress.org, June 27, 2024.

The London Gold Fix: A Brief Guide, by gainesvillecoins.com, coinweek.com, August 3, 2022.

The Treasury Is About To Launch a 9 Trillion Question Mark Into the Markets And Bond Vigilantes Are Likely To Push Rates Higher, by Austin Smith, 24/7 Wall Street, 247wallst.com, March 2, 2025.